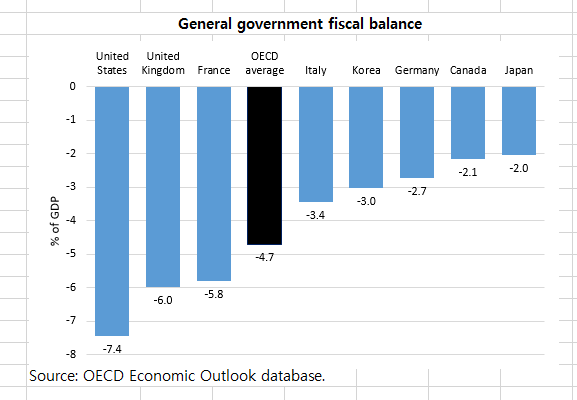

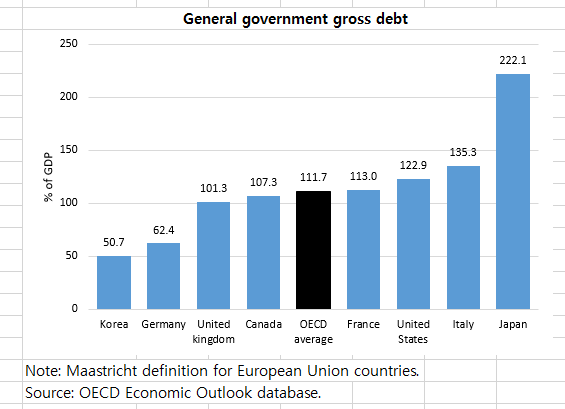

Government debt has risen markedly in most OECD countries over the past decades, reaching an average of more than 110 percent of GDP in 2024, nearly 40 percentage points above its 2007 level, prior to the global financial crisis (GFC). Within the seven major OECD economies, government debt ranged from 62 percent of GDP in Germany to 222 percent of GDP in Japan. In Korea, it slightly exceeded 50 percent of GDP. All big countries continue running budget deficits, from 2 percent of GDP in Japan to more than 7 percent of GDP in the United States, with Korea at 3 percent of GDP in 2024. Debt increased sharply during the GFC and the COVID-19 pandemic, and most governments failed to reduce significantly their debt ratios during economic expansions. Very low interest rates in the decade following the GFC alleviated the debt burden in most countries, substantially weakening incentives to reduce deficits.

However, over the past few years interest rates have risen, economic growth prospects have become more uncertain amid geopolitical tensions, and many governments have pledged to spend more on defense, especially in Europe. Several major economies have experienced bouts of tension in their government bond markets, including the United Kingdom and the United States. French government bond yields have risen and credit ratings have been downgraded, as the absence of a parliamentary majority hampers the adoption of a budget that would lower the government deficit from a level that exceeds 5 percent of GDP. With higher interest rates and heightened economic and political uncertainty, fiscal sustainability has forcefully reemerged in the policy debate in many OECD countries.

This is particularly the case in Europe, where the sovereign debt crisis of the early 2010s has left durable scars, even though the current financial situation in the euro area is nowhere near that of 2011-12, when Greek, Portuguese and Irish 10-year government bond spreads vis-à-vis Germany peaked at about 33, 12 and 10 percentage points respectively. As of October 28th, France, along with Italy, had the euro area’s highest 10-year government bond spreads with Germany, at around 0.8 percentage points. Countries involved in the euro sovereign debt crisis in the past decade then ran large external deficits, contrasting with France’s roughly balanced current account today, despite a deterioration in export performance compared to the pre-pandemic period. Furthermore, following Mario Draghi’s July 2012 speech in which he stated that the European Central Bank was ready to do “whatever it takes” to preserve the euro, mechanisms to deal with crises within the currency union have been considerably strengthened. In addition, structural reforms in several euro area countries have improved their fiscal positions and competitiveness, limiting contagion risks.

Nevertheless, there is no room for complacency. Defining a threshold at which government debt becomes dangerous is challenging and such a level would vary across countries. Japan has so far been able to finance a gross government debt of over 200 percent of GDP at a relatively low cost, thanks to abundant domestic savings flowing into government bonds and unconventional monetary policy, while lower debt levels proved unsustainable in euro area peripheral countries, which had to be bailed out by the “Troika” (European Commission, European Central Bank and International Monetary Fund) and implement tough adjustment programs. In any case, high debt increases the risk that investors lose confidence and push up interest rates, and may also hamper policy responses to economic shocks, worsening recessions and financial stress.

Without policy action, government debt is set to rise further in most OECD countries, as population aging pushes up pension, health and long-term care spending, which according to OECD long-term projections could increase by nearly four percentage points of GDP on average in the OECD by 2060, and about twice as much in Korea, which will experience the fastest rise in the share of the population aged 65 or over. Potential increases in defense spending, as geopolitical tensions mount, could further strain public finances in many countries.

Debt dynamics are crucially affected by developments in interest rates and output growth. For a given primary budget balance, which excludes net interest payments, debt increases if interest rates are higher than GDP growth and decreases in the opposite case. Although forecasting future interest rates is challenging, the long period of extremely low interest rates that followed the GFC seems over. Market-based indicators, such as yield spreads between 10-year and 30-year sovereign bonds, or 10-year forward real interest rates in 10 years, point to expectations of higher interest rates in the future. Meanwhile, the working-age population will grow more slowly over the coming decades and even shrink in more than half of OECD countries, including Japan, Korea and many European countries. This will pull down potential growth. Demographic headwinds could be partly offset by higher productivity growth, especially thanks to the diffusion of artificial intelligence. However, estimates of AI-related gains vary widely across studies and other factors, like rising obstacles to trade and heightened uncertainty may weigh on productivity growth. Stronger GDP growth would help reduce debt. Recent OECD research shows that growth has played a major role in almost all public debt reduction episodes in OECD countries since the 1970s. Governments should promote growth-enhancing reforms, while remaining prudent about growth projections embedded in fiscal plans given the uncertainties involved.

The rise in government debt is not inevitable. Among OECD countries, Estonia has the lowest government debt-to-GDP ratio, below 24 percent in 2024. Denmark and Sweden’s government debt ratios are now only slightly above 30 percent, after peaking around respectively 84 percent (in 1993) and 69 percent (in 1996), illustrating the potential of a strong commitment to fiscal responsibility to bring down public debt. The Scandinavian countries are efficient welfare states, ranking among the world’s happiest countries, showing that fiscal discipline does not need to come at a high social cost. Moreover, the ratio of tax and social contributions to GDP in these countries is now lower than when government debt ratios peaked. Many factors influence government debt developments. Lengthening working lives is crucial to contain pension costs and fostering high employment in all age groups can support economic growth and government revenue, particularly in aging societies. High productivity can generate additional resources. Efficiency gains can help contain public expenditure, including on health and long-term care.

A solid fiscal framework helps ensure that fiscal policy is both sustainable and responsive to economic conditions. Budget deficits can stimulate the economy in case of weak demand, limiting contractions in output and employment, mitigating scarring effects on the economy. However, fiscal buffers should be restored during expansions. Flexible fiscal rules, such as budget deficit caps over the business cycle rather than every year, allow policy responsiveness. But they are also more difficult than more rigid rules to implement. Many OECD countries have put in place independent fiscal “watchdogs” to inform fiscal and economic policy. For example, the Danish Economic Council and the Swedish Fiscal Policy Council play an important role in fiscal monitoring and policy analysis. While Korea’s government debt remains relatively low by OECD standards, it has grown rapidly in recent years and rapid aging will increase upward pressure. Strengthening the Korean fiscal framework would facilitate debt containment.

More generally, across the OECD, governments need to pursue prudent fiscal policies, as spending pressure from population aging is rising, uncertainty about interest rates and growth prospects has increased, climate change heightens the risk of costly natural disasters, economic fragmentation increases the probability of economic shocks and growing political polarization in many countries may hamper corrective action in case of deficit drift, triggering adverse market reactions.

Christophe Andre

Christophe Andre is a senior economist at OECD. The views expressed in this column are those of the author and not of the OECD or of its member countries. — Ed.

khnews@heraldcorp.com